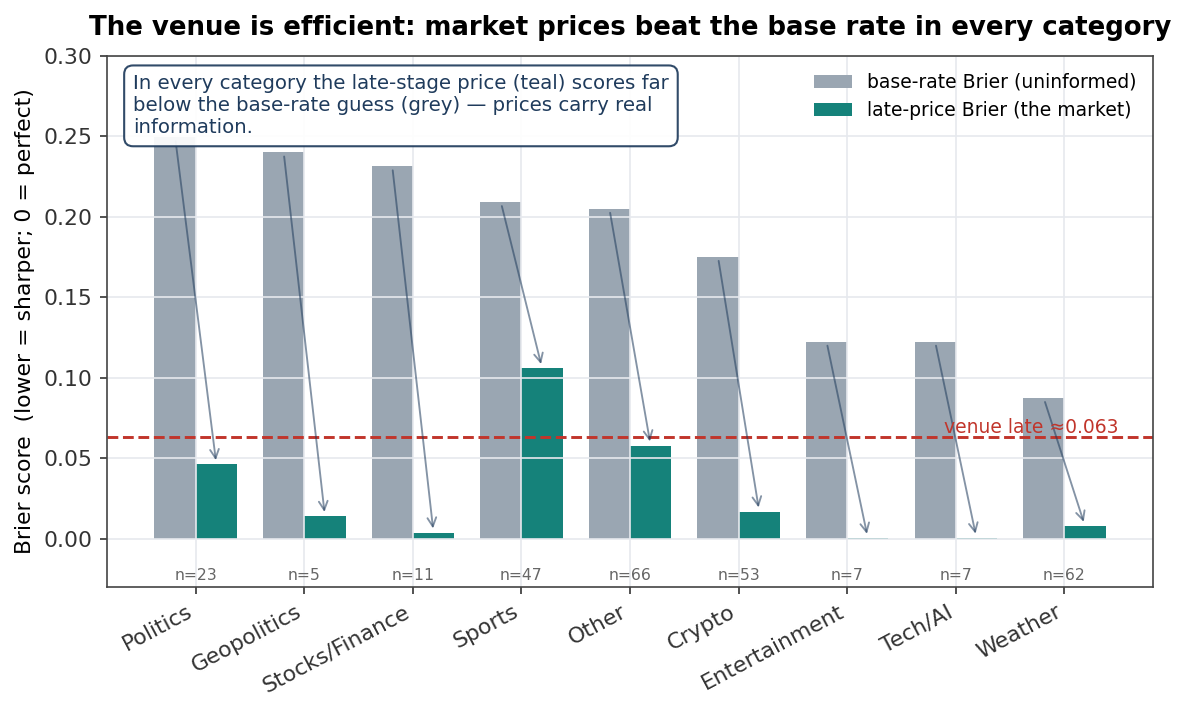

Exp 1 — Is the venue exploitable? (groundwork)

- Establish venue efficiency and the absence of a directional edge — the negative result that motivates studying dynamics.

- Five independent NO-EDGE findings; the market price beats every coarse prior tested.